|

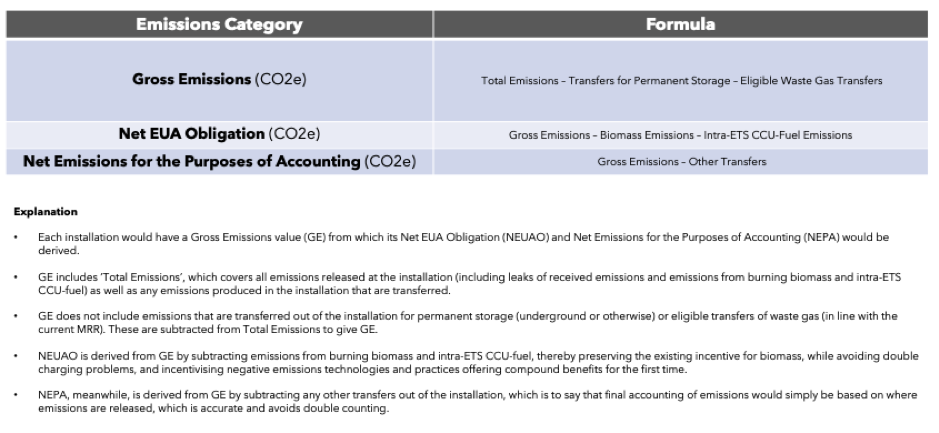

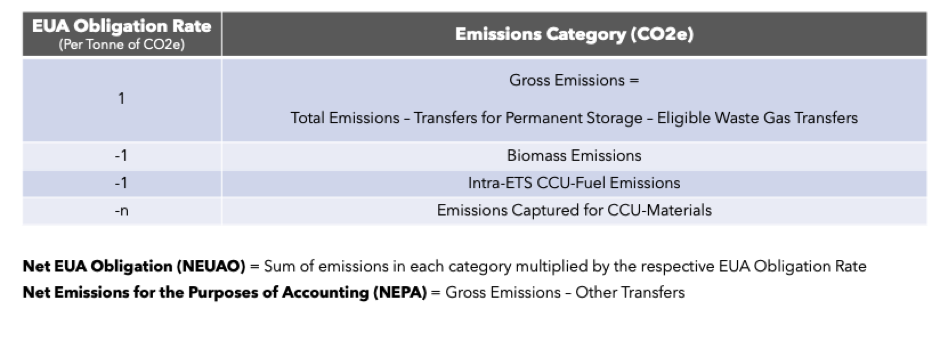

In a 2017 post we set out some guiding principles for accommodating CCU into the EU ETS, drawing on a report co-authored with André Bardow. Now seems like a good time to revisit the issue. Late last year, in response to an ECJ ruling, the European Commission revised the Monitoring and Reporting Regulation (MRR) to exempt emissions from the ETS that are transferred out of an installation for the purposes of making precipitated calcium carbonate (PCC). And this year the Commission is reviewing the MRR ahead of Phase IV, providing an opportunity to further accommodate CCU practices into the ETS. This has prompted a number of reports with recommendations in this area (e.g. Umweltbundesamt and CE Delft). Building on the principles in our original post, then, let’s consider how best to move forward with the MRR revision and potential revisions to the ETS Directive during Phase IV. 1. Implementing the ECJ ruling One of our immediate priorities should be implementing the aforementioned ECJ ruling in a way that does not create an incentive to move emissions outside the jurisdiction of the carbon price. As amended, the MRR currently provides a full exemption for emissions transferred out of an installation for the purposes of making PCC, despite the fact that PCC can go into a range of applications, some offering permanent storage and others not, and despite the fact that Annex 1 of the ETS Directive has not been revised to ensure that installations involved in transporting and processing these emissions are regulated by the ETS. This outcome reflects a problematic reading of the ECJ ruling, which has it that emissions are unreleased by the court’s reckoning when chemically bound in a stable product, such as PCC. This could open the door to exemptions across the board for CCU practices, even though they have very varied environmental performance (which often depends on very low-carbon electricity) and emissions are often released at the end-of-life stage where they are not subject to the carbon price. The ECJ ruling, however, does not say that all emissions captured for the purposes of making PCC (or, more generally, that are chemically bound in a stable product) are unreleased. It only says that it is wrong to presume that all emissions captured for the purposes of making PCC are released: which is very different. Indeed, the ruling makes clear that leakage en route or at the processing installation would constitute a release. And the ruling does not preclude end-of-life emissions being classed as a release. To protect the integrity of the ETS, therefore, the Commission should interpret ‘release’ in a strict sense to include all stages after capture, limiting exemptions to emissions that are permanently stored (e.g. through mineralisation) and adjusting Annex 1 to ensure that installations involved in transporting and processing such emissions are covered by the ETS. By contrast, the MRR revision should not be used to extend exemptions to CCU fuels and products more generally just because emissions are chemically bound in a stable substance. And the ECJ ruling—which concerns whether captured emissions are released—does not provide a legal basis or implicit methodology for calculating partial exemptions that would in fact derive their justification from counterfactual emissions savings cradle-to-gate in the value chain (cf. Umweltbundesamt). 2. Solving the CCU-fuel double-charging problem A second issue we must address is that the ETS would currently double charge for emissions if a CCU-fuel was made and burnt entirely within the ETS. To avoid this, the Commission could apply a zero-rate emissions factor for CCU-fuels burnt at ETS installations, provided the emissions used to make the fuel were captured and processed within the ETS. This could follow the approach taken with biomass currently and would be consistent with the interpretation of the ECJ ruling advocated above, which is to say that the captured emissions would not be exempted because they would be classed as ‘released’. Installations involved in transporting and processing emissions for use in CCU-fuel would have to be included in the ETS, and CCU-fuel produced within the ETS would need to be certified as such (distinguishing it from imported CCU-fuel). This seems much simpler than providing an exemption at the point of capture, which would require the capturing installation to prove that the emissions were later processed into a CCU-fuel that was burnt within the ETS. 3. Reforming accounting practices The proposed approach (exempting permanently stored emissions and avoiding double charging within the ETS) is consistent with existing ETS principles and does not require any adjustment to ETS or Effort Sharing Regulation (ESR) budgets. No additional EUAs/AEAs would be issued, and no exemptions would be provided in the ETS for counterfactual value-chain savings or savings in ESR sectors. But there are still accounting issues to deal with, because emissions captured in the ETS for CCU-materials and extra-ETS CCU-fuels would be counted in the ETS and at the end-of-life stage in the ESR. Furthermore, there is a systemic accounting problem that needs attention; namely that currently the ETS fails to incentivise negative emissions technologies and practices that deliver compound benefits such as BECCS. One solution would be to move to a gross-net accounting system in the ETS that distinguishes between an installation's EUA obligation and the emissions attributed to it for accounting purposes.  Table 1. ETS gross-net accounting Under such a scheme, an installation would have a Gross Emissions value (GE), which would comprise its total emissions, minus any transferred for permanent storage (underground or otherwise) and any transferred under existing MRR waste-gas rules. Total emissions, here, would cover all emissions released at the installation (including leaks of received emissions and emissions from burning biomass and intra-ETS CCU-fuel) as well as any emissions produced in the installation that were transferred. (To be clear, emissions from burning biomass and intra-ETS CCU-fuel would not be zero-rated when calculating GE.) An installation would then derive its Net EUA Obligation (NEUAO) by subtracting its biomass and intra-ETS CCU-fuel emissions from its GE. And it would separately derive its Net Emissions for the Purposes of Accounting (NEPA) by subtracting any additional transfers out of the installation from its GE (e.g. for making CCU-fuel or CCU-materials). This approach would: i) preserve the existing biomass incentives, ii) avoid intra-ETS CCU-fuel double charging, iii) prevent double counting by accounting for emissions where they take place, iv) improve the accounting for biomass emissions in the energy sector (currently done via LULUCF reporting), and v) provide incentives for negative emissions and practices with compound benefits for the first time. On this last point, installations with negative emissions (e.g. those conducting BECCS or DAC) would have to be added to Annex 1 and they would be issued EUAs in accordance with their negative NEUAO. The EUAs could come from a reserve under the existing ETS cap to ensure emissions reductions are additional rather than a form of offsetting. Now, double charging would happen under this system if emissions were captured from an installation for use in an application that did not offer permanent storage and the receiving installation leaked the emissions. But this is the only acceptable approach, because not charging for the leak at the second installation would create perverse incentives. (And the system would still correctly count the emissions once.) 4. Rewarding CCU value-chain savings None of the above is to say that CCU applications that don’t offer permanent storage cannot reduce emissions. It’s just that savings would be counterfactual value-chain savings. That is, a CCU value chain can emit less cradle-to-gate compared to a virgin fossil feedstock value chain. Let’s consider, then, how this sort of emissions avoidance could be incentivised within the ETS, which is currently set up to charge installations for their actual emissions. One option would be to modulate the EUA obligation at the installation capturing the emissions to reflect the estimated cradle-to-gate counterfactual saving (taking into account key factors such as the CCU application and energy mix). Modulating the attribution of emissions to the installation would create complications for accounting between the ETS and ESR, so accounting could be kept separate by distinguishing NEUAO and NEPA as above.  Table 2. Modulating EUA obligations The problem with this approach, though, is that it would fundamentally change the nature of the cap by exempting actual emissions based on counterfactual emissions savings. It would also be difficult to calculate the EUA Obligation Rates and burdensome to administer, requiring coordinated reporting between installations along value chains.

A better option might be to issue EUAs under Article 24(a) of the ETS Directive to projects that deliver counterfactual savings (or savings in non-ETS sectors). The EUAs could be sourced from the existing cap (or transferred from AEAs) to preserve the integrity of carbon budgets. Accounting could still be based on the NEPA approach outlined above, with estimation of counterfactual value-chain savings done separately by the project consortium purely as a condition for receiving credits. Nevertheless, developing project mechanisms under Article 24(a) is a big task and project participants would face significant administrative burdens. Given the current scope of the ETS, then, perhaps the best option is to explore other incentives for those CCU practices that do not offer permanent storage and where emissions are potentially released in non-ETS sectors. There are lots of options. As well as funding R&I and stimulating investment, we could look at quotas for alternative feedstocks in products, for instance, or price interventions to overcome barriers to the uptake of alternative feedstocks, such as CfDs. And in the long run we should consider incorporating end-of-life emissions in CCU value chains (e.g. from incineration) into the ETS so we can provide a simple exemption at the point of capture without undermining the actuality of the cap. For further information, please contact damien.green@perspectiveclimate.com

0 Comments

|